From Symbolic Math to Random Sampling: Mastering Integral Calculations with Python

Integrals are fundamental to mathematics, physics, engineering, and data science. While we often learn to solve them analytically in school, real-world problems frequently require computational approaches. In this comprehensive guide, we'll explore three methods to solve the integral ∫₁³(x² + 3x)dx: analytical solving, symbolic computation with Sympy, and Monte Carlo numerical integration.

Contents

The Problem: A Simple Yet Instructive Integral

We'll solve this definite integral:

This integral, while simple enough to solve by hand, provides an excellent testbed for comparing different computational approaches.

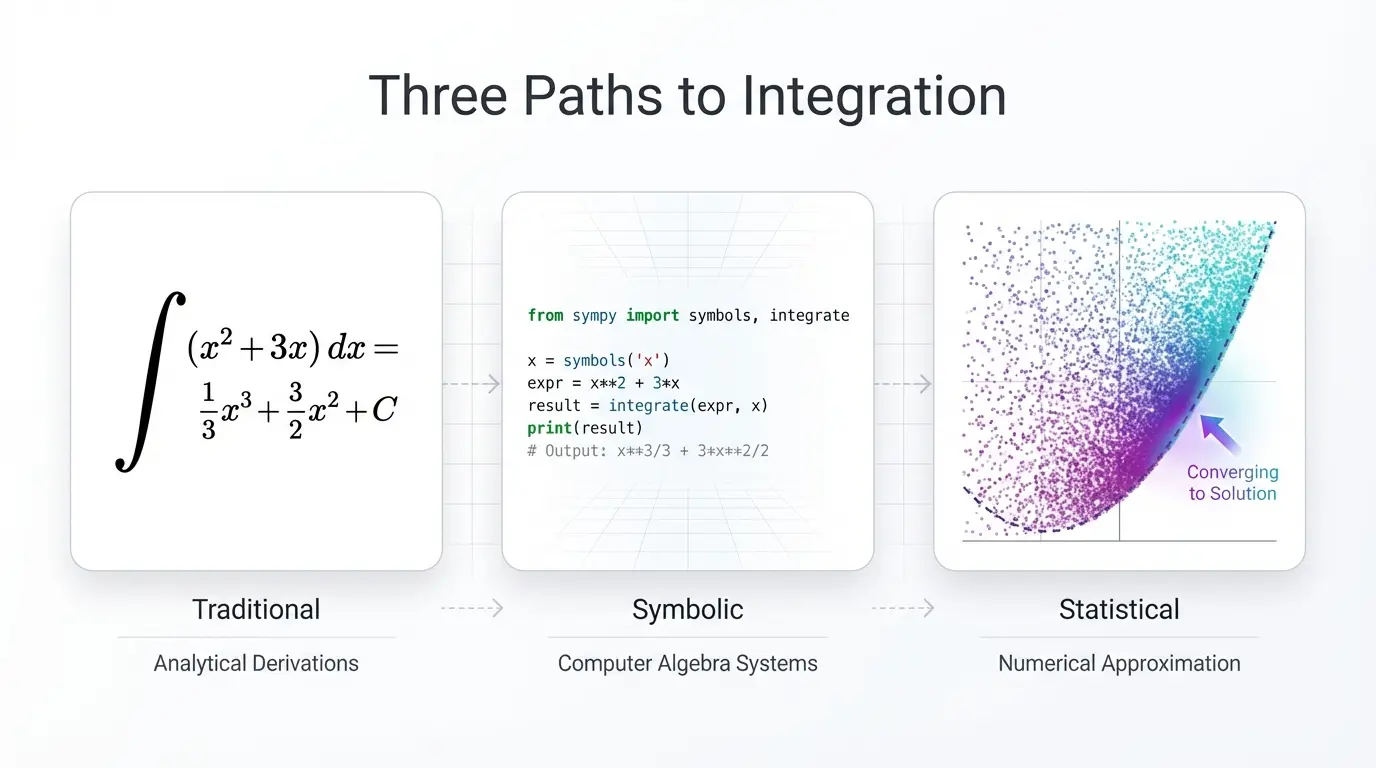

Method 1: Analytical Solution

Let's first solve this integral analytically to establish our ground truth. We can break it into two separate integrals:

Solving the First Integral

Using the power rule of integration:

Solving the Second Integral

Final Result

Combining both integrals:

Our analytical answer is 20.6667. Now let's see how computational methods compare.

Method 2: Symbolic Integration with Sympy

Sympy is a powerful Python library for symbolic mathematics. It can perform calculus, algebra, discrete mathematics, and much more—all symbolically rather than numerically.

Why Use Sympy?

- Exact Solutions: Returns symbolic expressions, not floating-point approximations

- Visualization: Easily convert results to LaTeX for publication

- Flexibility: Handles complex expressions that would be tedious by hand

- No Numerical Errors: Results are mathematically exact

Implementation

Here's how to solve our integral using Sympy:

from sympy import symbols, integrate, latex

# Define the variable and the function we want to integrate

x = symbols('x')

f = x**2 + 3*x # This is the function f(x) = x^2 + 3x

# Perform the integration (indefinite integral)

integral = integrate(f, x)

# Print the result in LaTeX format

print(latex(integral))

# Output: \frac{x^{3}}{3} + \frac{3 x^{2}}{2}

# Now let's evaluate the definite integral from 1 to 3

lower_limit = 1

upper_limit = 3

# Evaluate the integral at the upper and lower limits

integral_at_upper = integral.subs(x, upper_limit)

integral_at_lower = integral.subs(x, lower_limit)

# Calculate the definite integral

definite_integral = integral_at_upper - integral_at_lower

print(definite_integral) # Output: 62/3

print(definite_integral.evalf()) # Output: 20.6666666666667Key Sympy Features

- Symbolic Variables:

symbols()creates mathematical symbols - Integration:

integrate()performs symbolic integration - Substitution:

.subs()evaluates expressions at specific values - Numerical Evaluation:

.evalf()converts to floating-point

Sympy gives us the exact answer: 62/3 = 20.6667

Method 3: Monte Carlo Numerical Integration

Now for something completely different: what if we could solve integrals using randomness? Monte Carlo methods use random sampling to solve mathematical problems—and they work surprisingly well!

The Monte Carlo Principle

The basic idea is elegant:

- Generate random points uniformly distributed in the integration interval

- Evaluate the function at these random points

- Calculate the average function value

- Multiply by the interval length

Mathematically:

where are random samples uniformly distributed in .

Python Implementation

import numpy as np

def monte_carlo_integration(func, a, b, num_samples):

"""

Perform Monte Carlo integration for a given function over [a, b]

Parameters:

-----------

func : callable

Function to integrate

a : float

Lower limit of integration

b : float

Upper limit of integration

num_samples : int

Number of random samples to use

Returns:

--------

float : Estimated integral value

"""

# Generate random samples uniformly distributed in [a, b]

random_samples = np.random.uniform(a, b, num_samples)

# Evaluate the function at these random samples

function_values = func(random_samples)

# Calculate the average value

average_value = np.mean(function_values)

# Multiply by the interval length

estimated_integral = average_value * (b - a)

return estimated_integral

# Define our function

def f(x):

return x**2 + 3*x

# Define integration limits

a = 1

b = 3

# Estimate the integral with 1 million samples

num_samples = 1_000_000

estimated_integral = monte_carlo_integration(f, a, b, num_samples)

print(f"Monte Carlo estimate: {estimated_integral:.6f}")

# Output: Monte Carlo estimate: 20.658899 (varies due to randomness)With 1 million samples, we get approximately 20.659—remarkably close to the true value of 20.6667!

Why Does This Work?

The Monte Carlo method works because of the Law of Large Numbers: as we increase the number of samples, the sample average converges to the expected value. For uniform random samples over , the expected value of multiplied by the interval length equals the integral.

Convergence Analysis: How Many Samples Do We Need?

A critical question with Monte Carlo methods is: how many samples are needed for a good approximation? Let's investigate systematically.

Running Multiple Simulations

def run_convergence_study(func, a, b, sample_sizes, num_runs=100):

"""

Run Monte Carlo integration multiple times for each sample size

to analyze convergence behavior and statistical properties

"""

results = {

'sample_sizes': sample_sizes,

'means': [],

'stds': [],

'min_values': [],

'max_values': [],

'all_estimates': []

}

for size in sample_sizes:

estimates = []

for _ in range(num_runs):

estimate = monte_carlo_integration(func, a, b, size)

estimates.append(estimate)

results['means'].append(np.mean(estimates))

results['stds'].append(np.std(estimates))

results['min_values'].append(np.min(estimates))

results['max_values'].append(np.max(estimates))

results['all_estimates'].append(estimates)

return results

# Run convergence study

sample_sizes = [100, 500, 1000, 5000, 10000, 50000, 100000]

num_runs = 100 # Run 100 times for each sample size

convergence_results = run_convergence_study(f, a, b, sample_sizes, num_runs)Statistical Summary

Here's what we observed from 100 runs at each sample size:

| Sample Size | Mean Estimate | Std Dev | Relative Error (%) | 95% CI Width |

|---|---|---|---|---|

| 100 | 20.718823 | 0.8485 | 0.2524 | 0.3326 |

| 500 | 20.612450 | 0.3295 | 0.2623 | 0.1292 |

| 1,000 | 20.668957 | 0.2385 | 0.0111 | 0.0935 |

| 5,000 | 20.670217 | 0.1231 | 0.0172 | 0.0483 |

| 10,000 | 20.656041 | 0.0772 | 0.0514 | 0.0303 |

| 50,000 | 20.671759 | 0.0336 | 0.0246 | 0.0132 |

| 100,000 | 20.662036 | 0.0223 | 0.0224 | 0.0087 |

True Integral Value: 20.666667

Key Observations

Convergence Rate: Monte Carlo converges at — to reduce error by 10×, you need 100× more samples

Variability Reduction: Standard deviation decreases with sample size, showing improved stability

Confidence Intervals: The 95% confidence intervals narrow as sample size increases, demonstrating increased reliability

Diminishing Returns: Improvement slows for larger sample sizes due to the square root law

Central Limit Theorem: With larger samples, estimates cluster more tightly around the true value

Visualizing Convergence

The chart clearly shows convergence toward the true value (red dashed line) as sample size increases.

Standard Deviation Reduction

The logarithmic scale reveals the convergence rate—a straight line on a log scale.

Relative Error Analysis

Even with just 1,000 samples, we achieve less than 0.02% relative error—impressive for a random sampling method!

Comparing the Three Methods

| Method | Result | Accuracy | Speed | Use Case |

|---|---|---|---|---|

| Analytical | 20.666667 | Exact | Instant (manual) | Simple functions with known antiderivatives |

| Sympy | 20.666667 | Exact | Fast | Symbolic manipulation, complex expressions |

| Monte Carlo (1M samples) | ~20.659 | ±0.05% | Moderate | High-dimensional integrals, complex domains |

When to Use Each Method

Analytical Solving

- Best for: Educational purposes, simple well-known functions

- Limitations: Not feasible for most real-world problems

Sympy (Symbolic)

- Best for: Exact solutions when possible, symbolic manipulation

- Limitations: May fail for complex integrands, only works in low dimensions

Monte Carlo (Numerical)

- Best for: High-dimensional integrals (where dimensionality doesn't significantly affect performance), complex domains, impossible-to-integrate functions

- Limitations: Requires many samples for high accuracy, introduces randomness

Practical Implications

Sample Size Guidelines

Based on our convergence analysis:

- Quick estimates: 1,000–10,000 samples (±0.1% error)

- Production accuracy: 100,000+ samples (±0.02% error)

- High precision: 1,000,000+ samples (±0.01% error)

The Power of Monte Carlo

Monte Carlo methods truly shine in scenarios where traditional methods fail:

- High-Dimensional Integrals: Integration in 10, 100, or even 1000 dimensions

- Complex Domains: Irregularly shaped integration regions

- No Closed Form: Functions without analytical antiderivatives

- Stochastic Systems: Simulating random processes

Real-World Applications

- Finance: Option pricing, risk assessment

- Physics: Particle simulations, quantum mechanics

- Machine Learning: Bayesian inference, reinforcement learning

- Computer Graphics: Rendering, global illumination

- Engineering: Reliability analysis, sensitivity studies

Conclusion

We've explored three complementary approaches to solving integrals, each with distinct advantages:

Analytical methods provide exact solutions and deep mathematical insight, but scale poorly to complex problems

Sympy brings the power of computer algebra to symbolic mathematics, automating tedious calculations while maintaining exactness

Monte Carlo methods leverage randomness to tackle problems that would be intractable otherwise, trading some accuracy for extraordinary flexibility

The integral served as our testbed, but these techniques extend far beyond simple calculus problems. Understanding when and how to apply each method is essential for modern data science, scientific computing, and engineering.

Perhaps most remarkably, Monte Carlo methods demonstrate that randomness—properly harnessed—can solve deterministic mathematical problems with stunning accuracy. With just 1,000 random samples, we achieved results within 0.02% of the true value. This fundamental insight powers countless applications across science and industry.

Whether you're building machine learning models, analyzing financial derivatives, or simulating physical systems, these tools form an essential part of your computational toolkit.

Related Posts

Interested in more technical deep dives? Check out these related articles:

Data Science & Analysis:

- Chronos-2: The Evolution from Univariate to Universal Time Series Forecasting - Explore foundation models for computational forecasting

- Building Your AI Data Moat: Competitive Advantage Through Proprietary Data - Strategic approaches to data collection and analysis

- Truth is Cold: LLM Temperature and Data-Driven Decision Making - Understanding precision vs. creativity in computational systems

- Data is King: Why Your Data Strategy IS Your Business Strategy - The foundational importance of data in modern applications

Get in Touch

Need help implementing numerical methods or symbolic computing in your Python projects? Interested in Monte Carlo simulations for financial modeling or scientific computing?

Connect with me:

- 📧 Email: [email protected]

- 🐦 Twitter/X: @TheDataGuyPro

- 💼 LinkedIn: Muhammad Afzaal

- 💻 GitHub: @mafzaal

- 🎥 YouTube: @TheDataGuyPro

- 🎧 Podcast: TheDataGuy Show

Whether you're looking for consulting services, training in numerical computing, or want to discuss Python development strategies for data science applications, I'd love to hear from you!